Floating offshore wind an essential component of decarbonisation efforts

It is expected to be a driving force to change the energy paradigm from a largely fossil fuel-driven energy system to one based on renewables.

With COP 26 and the Paris Agreement strengthening the global response to climate change, countries around the world are facing increasing pressure to phase out carbon-intensive fuels in favour of clean energy.

Onshore and offshore wind power, especially large-scale floating turbines, can play a leading role in the clean energy revolution, with global capacity expected to increase tenfold in a little over a generation.

Falling hardware prices and growing confidence from investors have seen onshore wind farms become a popular and cost-effective solution. Fixed offshore technology is also maturing at a significant pace and will be an important part of the new energy mix. However, as fixed offshore wind turbines need to be sited in relatively shallow water (with depths of up to 60 metres), their scope is limited.

With higher capacity factors compared to onshore wind or solar, offshore wind provides greater energy reliability to emerging markets where power demand is growing, especially if aggregated over large geographical areas.

To access the huge potential of offshore wind globally will require large-scale, floating facilities. This technology has the potential to harness wind power at greater ocean depths, providing large-scale renewable power to help countries meet ambitious decarbonisation targets.

New versions of floating wind turbines and seabed moorings can tap wind power in water depths of over 50m or more, opening up large swathes of deepwater zones to renewable power generation for countries that have limited onshore space for large-scale solar or wind.

For example, deep waters and strong winds make Japan one of the most attractive countries in the world for commercialising floating wind energy. Once floating wind technology has moved past the demonstration stage to become commercially viable, Japan expects to add over 1GW per year of the technology up to 2040.

Growth potential

Through technological innovation and economies of scale, the global wind power market has nearly quadrupled in size over the past decade and established itself as one of the most cost-competitive, resilient and low emissions power sources in the world, according to the Global Wind Energy Council (GWEC).

Over 733 GW of total wind generation capacity has been installed worldwide as of end-2020 of which 95% is onshore wind and the remaining 5% offshore wind. The vast majority of total installed capacity is located in Asia (322 GW) followed by Europe (208 GW), North America (139 GW) and 54 GW in the rest of the world.

As of end-2020, China led in overall installations with 282 GW, followed by the United States (118 GW), Germany (62 GW) and India (39 GW).

Offshore wind has enjoyed a bumper year globally in 2020, driven by a surge of renewable energy capacity auctions, favourable feed-in tariffs (FITs) in countries such as

China and a 67% reduction in the levelised cost of high-performance, thanks to giant offshore wind turbines, according to BloombergNEF. The first half of 2020 alone saw US$35 billion allocated in financing to offshore wind, a rise of 319% year-on-year and well above 2019’s full-year figure of US$31.9 billion.

Despite the COVID-19 pandemic denting electricity demand, nearly 100 GW of new wind generation capacity was installed worldwide in 2020 - a 59% year-on-year increase - driven by a surge of installations in China and the US. The world’s two largest wind power markets installed nearly 75% of new installations in 2020 and now account for over half of the world’s total wind power capacity.

This year looks set to be another record year. In the first half of 2021, nearly 7 GW of wind power capacity was auctioned globally, a 160% year-on-year increase compared to Q1 2020. With 3.9 GW awarded in Q1 2021, offshore wind accounted for the majority of the sanctioned wind power capacity.

This year and next, the IEA is predicting that global offshore wind capacity additions will increase 60% to over 10GW, with China expected to account for nearly 60% of this as developers rush to take advantage of FITs before they expire at end-2021.

In Asia, Japan and Korea are also set to commission smaller projects for the first time in 2022.

Both Japan and Korea have implemented initiatives aimed at supporting floating offshore wind. In Japan, a feed-in-tariff is available for floating wind projects while an auctions scheme has been implemented for fixed bottom projects.

In June, the proposal for a 16.8 MW floating wind farm off the coast of Goto City in Nagasaki Prefecture was confirmed in Japan’s floating wind auction. Once built, this will be the country’s first commercial floating offshore wind farm. The coast of Goto City has a water depth of 100 m – 150 m which will require floating solutions as fixed substructures will not be economical at such depths.

In South Korea, additional RECs are awarded for every MWh of offshore wind generation compared to onshore renewables like solar and onshore wind. However, investors are still seeking clarity on guidelines and are pushing for additional support.

Ulsan in South Korea has been receiving much attention as a floating wind hub with the numerous collaborations observed between international investors and local developers.

In Taiwan, additional subsidies for floating wind projects are currently not available. As such, the bulk of the initial applications for the upcoming round 3 auctions which focuses on projects from 2026 onwards are expected to be based on fixed bottom technology. The round 3 auctions will be highly competitive and will most likely be oversubscribed. Taiwan’s offshore wind allocation plan for 2026-2035 proposes a total of 15 GW of new capacity to be added.

For China, most offshore wind projects are still focused on shallow water where fixed bottom installations are suitable. While a floating wind turbine was installed this past July off the coast of Guangdong Province, it was deployed mainly for demonstration purposes. Commercial-scale deployments of offshore floating wind (>1GW) are only expected after 2030. Initial plans for such projects are being considered in the Qingdao area.

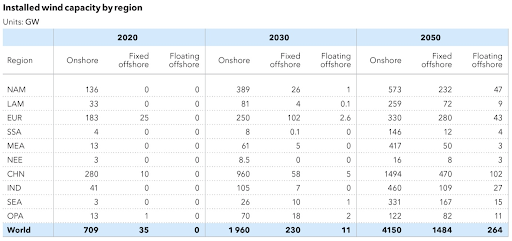

By 2050, up to 50% of floating wind capacity demand is expected to come from Asia Pacific countries as decarbonisation efforts across the region gather pace.

According to the International Energy Agency (IEA), the offshore wind energy market is expected to grow faster than the onshore wind sector, driven by rising cost-competitiveness, with an average LCOE of US$50/MWh being within reach.

The International Renewable Energy Agency (IRENA) forecasts global weighted average capacity factors for onshore wind will increase to 32-58% by 2050 and to 43-60% by 2050 for offshore wind.

Such is the potential and growing appetite for large-scale offshore wind that DNV’s Energy Transition Outlook predicts that it will make up 20% of all offshore wind resources by 2050. This implies a capacity of 250 GW by the middle of this century compared to just 34 GW today.

With each doubling of installed capacity, offshore wind costs fall by around 16%, a cost learning curve driven by technology improvements, more effective manufacturing, economies of scale, broader supply chain efficiencies and competition.

DNV expects nine capacity doublings between now and 2050 for floating offshore wind, which will see costs fall to around €40 (US$ 47) per MWh. Most of these doublings in capacity will take place over the next decade which will be when most cost benefits are realized. Within 10 years, DNV expects that offshore floating wind will be close to half of today’s cost levels.

Demonstration to commercialisation

Getting large-scale floating wind generation to a bankable scale will require a coordinated effort from governments, regulators, investors, developers, shipyards and customers.

It will also require consolidation and maturing of the complex technology required for various components, including the foundations (floaters) which sit on the water’s surface. Finding ways of mounting a tower and turbine in deep water environments is where most R&D is currently focused.

There are also engineering and modelling challenges associated with concrete versus steel foundation structures, wave and wind motion and load variables, network stability and transportation issues associated with supplying power into the onshore grid.

Around 40 different floater designs are being explored with four basic technologies at a commercial or pre-commercial stage: floaters with spar, semi-submersibles, barge-mounted turbines and tension-leg platforms. Determining which ones will become the dominant technologies – some of which may be suited to specific areas such as typhoon zones - will be critical in advancing the sector to a commercial stage.

Thereafter, standardisation of design concepts and certification against an agreed standard will be required to build stakeholder confidence in the technology and move to mass production. Collaboration and integration across domains will also be needed to

build an effective supply chain and create a thriving industry involving turbine manufacturers, shipyards, cable manufacturers and substation providers.

Spar and Semi-Sub are popular architectures in Asia and are being considered by a number of international developers who are strong advocates of these technologies.

In the offshore space, the oil and gas sector’s long-standing experience of deep-water conditions is a major advantage, coupled with their significant balance sheets and an incentive to transition to cleaner business models.

There are early signs that energy majors are looking at repurposing the oil and gas space for the floating offshore wind sector, leveraging their understanding of floaters, substrate structures, anchoring and offshore power interconnectors.

Floating wind power is expected to be a driving force to change the energy paradigm from a largely fossil fuel-driven energy system to one based on renewables, enabling offshore wind to make up a significant share in the global energy mix by 2050.

As the push for hydrogen-driven societies gathers pace, large scale floating wind could be used to produce electricity which in turn could be used to produce hydrogen for export. In this regard, the repurposing of offshore oil and gas platforms in regions such as Australia’s Bass Strait could form part of a hydrogen export infrastructure system.

DNV looks forward to continuing working closely with stakeholders across industries to accelerate floating offshore wind development which offers much potential for space-constrained nations to achieve carbon neutrality while meeting growing power needs close to demand centres.

For more information on DNV’s offshore and onshore wind power capabilities, please visit: www.dnv.com/power-renewables/generation/wind-energy.html

Global Wind Capacity Forecast

DNV Energy Transition Outlook 2021 Report

The original article is co-written by:

Legend:

North America (NAM) – United States and Canada

Latin America (LAM) – the region stretches from Mexico to the southern tip of South America

Europe (EUR) – all European countries including the Baltics but excluding Russia, all the former Soviet Union Republics and Turkey

Sub-Saharan Africa (SSA) – the region consists of All African countries except Morocco, Algeria, Tunisia, Libya and Egypt

Middle East and North Africa (MEA) – Morocco to Iran, including Turkey and the Arabian Peninsula

North East Eurasia (NEE) - Russia, Mongolia, North Korea and the former Soviet Union states except the Baltics

Greater China (CHN) – Mainland China, Taiwan, HK, Macau

Indian Subcontinent (IND) – India, Pakistan, Afghanistan, Bangladesh, Sri Lanka, Nepal, Bhutan and the Maldives

South East Asia (SEA) – region stretches from Myanmar to Papua New Guinea and includes the Pacific Ocean States

OECD Pacific (OPA) – Australia, New Zealand, Japan and South Korea

END

¹ gwec.net/global-wind-report-2021

² p25: www.irena.org/-/media/Files/IRENA/Agency/Publication/2021/Apr/IRENA_RE_Capacity_Statistics_2021.pdf

³ https://about.bnef.com/blog/global-wind-industry-had-a-record-near-100gw-year-as-ge-goldwind-took-lead-from-vestas

⁴ https://gwec.net/wind-power-auctioning-bounces-back-with-160-year-on-year-rise-in-q1-2021

⁵ dnv.com/Publications/the-unstoppable-rise-of-floating-offshore-wind-episode-1-196832

⁶ irena.org/-/media/Files/IRENA/Agency/Publication/2019/Oct/IRENA_Future_of_wind_2019_summ_EN.PDF

⁷ dnv.com/energy-transition/index.html

Advertise

Advertise